Remember that nice little rally from mid-June until somewhere around mid-August, when the market returns seemed to be moving us out of bear market territory? We don't either; that little upturn seems like a long time ago.

The past month and a half re-established the down-market trend that has generally been going on since the start of the year, as the markets gave back everything they had gained since the rally from their June 15 lows. The widely quoted S&P 500 index of large company stocks lost 5.28% in the third quarter and is down 24.77% so far this year.

The Russell 2000 Small-Cap Index is down 25.10% in the year's first nine months, and the technology-heavy Nasdaq Composite Index is showing a 33.20% loss so far this year, as tech stocks continue to experience greater downdrafts than the market as a whole.

International investors are sharing our pain. The broad-based EAFE index of companies in developed foreign economies lost 10.01% in the third quarter, and now stands at a negative 28.88% return for the year so far. Emerging market stocks of less-developed countries also joined in the global decline, falling 12.48% in dollar terms in the third quarter, down 28.91% for the year.

Looking over the other investment categories, real estate, as measured by the S&P U.S. REIT index, posted a 10.83% loss during the year’s second quarter, and is now down 29.99% since January 1. The S&P GSCI index, which measures commodities returns, lost 14.31% in the third quarter, but for the year is still showing an 8.30% gain.

In the bond markets, yields are continuing their rise that’s been going on since January. Shorter-term Treasuries with maturities ranging from 6 months to five years are all sporting yields of more than 4% for the first time in many years.

While rising rates have caused a lot of pain this year, the silver lining is that fixed income investors, including retirees, can finally look forward to earning a decent return on their safe money. Money market funds are paying close to 3%, and opportunities are now abundant. Thus, if you have money wasting away in bank accounts earning 0.05%, the time is ripe to move it somewhere more productive, without giving up any safety of principal. Give us a call if you want some advice on your own situation.

Despite the down market starting its tenth month, we aren’t out of the woods yet with this bear market in stocks, although it seemed like we might be getting there with the brief runup in stocks through mid-August. Market downturns come in all shapes and sizes, from the startling losses during the early COVID pandemic followed by a quick recovery, to what many of us regard as the most difficult kind to bear: the slow drip of down market days over a longer period of time.

The good news is that most individual investors have a longer-term view, and it is possible to peek over the horizon and see the day when inflation finally returns to its long-term norm, the Federal Reserve Board stops raising interest rates, and the economy recovers its equilibrium. There is no reason to think that the companies that make up the U.S. and global stock markets are now 25% less valuable today than they were last December–and, in fact, every reason to believe that the millions of people who go to work every day at those companies are continuing to add daily incremental value despite the pessimism of short-term traders.

Why have they become pessimistic? One reason might be found in the framing that the press has been giving recent economic news. In a recent example, the companies in the S&P 500 are growing their earnings at a 2.9% rate over the past three months–which you and I might think means that they are becoming more (not less) valuable. But the investment press focused on the fact that economists had been predicting higher growth, and that the current growth rate in earnings is slower than it has been over the past six or seven quarters.

Another example is rising wages: Salary.com recently reported that the median annual pay increase for American workers has risen to 4%, and hourly earnings overall are up 5.2%. This, of course, is the result of a high employment rates–and one might imagine that these are positive trends for the health of the U.S. economy. Instead, as you may have noticed in your own reading, these developments are framed as a headwind for the companies that have had to reverse the decades-long trend of suppressing their salary structures. Indeed, many of those companies are bringing manufacturing jobs back to the U.S., where they have to pay more for their labor than they did at overseas facilities. Have you read, anywhere, that the U.S. has added 461,000 new manufacturing jobs in this year alone? Didn’t think so.

Economists spend a lot of time trying to explain these downturns based on economic fundamentals, but in extreme market events, they throw up their hands because the fundamentals don't match what's going on. The better explanation is that both bull and (today) bear markets are psychological events. Humans are, in many ways, herd animals. When the herd moves in one direction or another, there is a strong tendency to move with it–to buy when others are buying, to sell when others are selling. Members of the investment press are no different; when the markets are going down, you might be tempted to imagine, from the articles you read, that the trend will continue until it takes stock prices all the way down to zero–a 100% decline. But we all know in which direction the next 100% movement will be; we have seen the aggregate markets go up 100% from many starting points, many times in history, and never once 100% in the other direction.

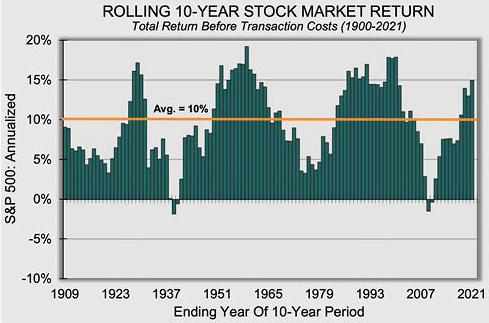

It bears repeating that there are no guarantees in the investment world, but history suggests that market downturns represent a buying opportunity for the long-term, and that markets tend to overshoot the actual underlying conditions on the upside and (alas) also on the downside. There is an unfortunate tendency that we all share, where we look at recent history and somehow convince ourselves that it was obvious all along. But the future is always cloudy; we look ahead to the next month or two and have no idea what is going to happen. We look out a bit further, however, and we see that there have been only two 10-year periods since 1941 where investors experienced a negative return–and those losses were very small.

In fact, if you look at the chart showing rolling 10-year returns in the S&P 500, you see the danger in thinking that any of us know how to dart in and out of the markets. The relatively brief downturns are followed by sudden, unexpected, impossible-to-predict reversals, and the biggest danger to wealth is not suffering a short-term paper loss but locking in a real loss and then missing the recovery.

Patient investors will accept the paper losses as a temporary blip in a long-term uptrend and the truly excellent investors will rebalance back to their original allocations, raising their exposure to stocks now that stocks are cheaper. If history holds, they will ultimately experience a recovery and no diminishment of their portfolios' buying power. The difference between a rapid ‘V'-shaped downturn like the one we experienced in the spring of 2020 and this kind of slow drip bear market is that what we are experiencing now makes that patience difficult to maintain. The slow drip will cause some investors to unbuckle their seat belts and jump off the market roller coaster before it has reached the end, and history has amply shown that that kind of panicked decision never ends well.